[Real-Estate] Home-Loans in Japan are Ridiculously Cheap - How to Take Advantage of Them

With variable-rate morgages still as low as 0.3%, Japan has the cheapest rates in the world! In this post, I cover why and how you can apply for one

*The terms “home-loan” and “mortgage” are used indiscriminately in this article

Table of Content

Click on each title to go straight to that section

1. Why home-loan rates are increasing rapidly worldwide

The world has seen the highest inflation in decades which have pushed central banks to raise interest rates to new heights. The US central bank, the Federal Reserve, has raised its interest rates to 4% and it’s predicted to reach 4.5% in the coming months.

This has had a tremendous effect on home-loans. The interest rate on an average 30-year fixed-rate mortgage have gone from 3% to over 7% just this year. That’s a 130% increase in interest payments for new home-buyers!

In Europe, variable mortgages are more common, which means that homeowners are already getting crushed by rising interest payments.

In my home-country of Sweden, interest rates have climbed from 1% to 4% this year, meaning that the average homeowner’s interest-rate payments have increased by 300% since January (SBAB Swedish home-loan newsletter)!

In the UK, interest-rates are forecasted to rise well beyond the average household’s disposable income, which will likely result in a massive increase of personal bankruptcies.

2. Why home-loans are so cheap in Japan

While housing markets worldwide have begun to collapse, the Japanese housing-market is doing just fine.

With inflation modest compared to other nations and the economy still below pre-pandemic levels, the Bank of Japan (BOJ) has signaled that there are no plans to tweak its pledge to keep rates at current or lower levels.

Despite Japan’s ultra-low interest rate environment, fixed-rate mortgages have increased in the last 10 months, indicating that Japanese banks are not completely insular to global inflation pressures, but compared to other countries, mortgage-rates are still very low.

If you go on Japan’s No.1 home-loan website, Kakaku.com, you’ll likely cry your eyes out if have a home-loan from another country…

For morgages with variable interest-rates, you can still get rates under 0.3%!

A. Most popular variable-rate mortgages in Japan:

Even for 30-year fixed-rate morgages, the rates are ridiculously low.

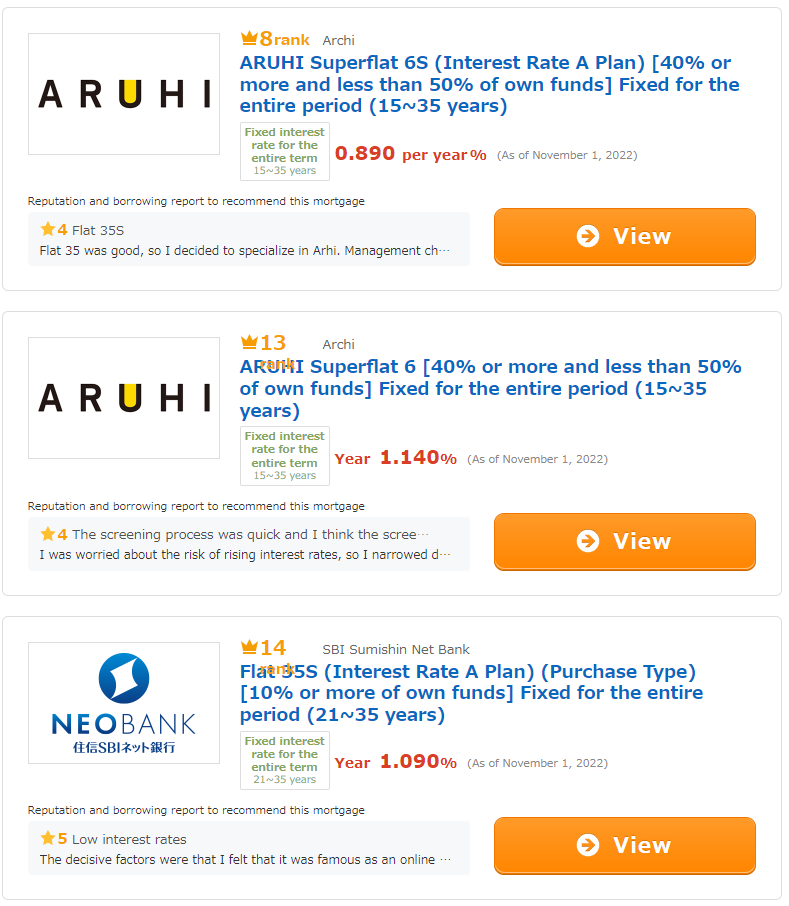

B. Most popular 26-35 years fixed-rate morgages in Japan:

It seems that even long-term, Japanese banks are certain that inflation and interest rates will remain low.

3. How to qualify for a Japanese home-loan as a foreigner

In Japan, there are basically no restrictions on foreigners purchasing Japanese real estate. Importantly, taxes on real-estate are levied in the same way as Japanese nationals, and there are no taxes levied only on foreigners.

Even if you’re a foreign national and do not have permanent residency, or even if you do not have any type of visa, you can still purchase real-estate in Japan.

Therefore, with the increase in the number of foreigners working in Japan, there are more and more cases of non-Japanese nationals purchasing homes in Japan.

A. Requirements for permanent residents

When a foreign national applies for a mortgage in Japan, the bank checks various personal information including annual income and length of employment. Of all the information, the most important is whether or not the applicant has permanent residency in Japan. The reason for this is that Japanese banks have a limited ability to collect outstanding loans if the applicant returns to their own country.

If the applicant has a permanent residence visa in Japan, most Japanese banks will assume that they have the same ability to pay back their loans as Japanese nationals and offer the same interest-rates and requirements.

B. Requirements for non-permanent residents

Most banks require foreigners to have permanent residency in Japan for applying for a mortgage.

However, there are more financial institutions than ever that accept non-permanent residents. If you want to apply for a mortgage without permanent residency in Japan, the screening process will be more difficult.

These are the main points to consider:

Years of residence: Usual requirement is that you have resided in Japan for more than 5 years.

Minimum annual income: Most often > JPY 5 million

Amount of down-payment: At least 20% of the property price, or more depending on your workplace and your annual income.

Japanese language ability: You or your guarantor must be able to understand Japanese to the extent that you understand all contract details (on rare occasions, contracts can be provided in English)

As a last resort, if you do not have permanent residency and cannot get a home-loan from a Japanese bank, you can consult with a foreign non-bank or your home country bank which has a Japanese branch. However, the interest rates are likely higher than those of Japanese financial institutions, and a larger down-payment is usually required.

4. Best Japanese home-loan banks for foreigners

Below, I have listed the most foreign friendly banks for home-loans for permanent & non-permanent residents.

Prestia SMBC Trust Bank is one of Japan’s biggest banks and is known for being foreign friendly with English support both online and in some of its physical locations. The bank also offers home-loans for non-permanent residents.

Mortgage page: "Prestia SMBC Trust Bank Housing Loans" [EN]

Requirements: Permanent residents, but also foreign nationals without permanent residency (excluding short-term visitor). Foreign applicants must have a stable source of income and a minimum annual income of JPY 7 million.

Maximum loan: JPY 1 million to 100 million.

Shinsei Bank is known for being foreign friendly with English support both online and in some of its physical locations.

Mortgage page: "Power Smart Mortgage" [EN]

Requirements: Permanent residence permit. However, if you do not have a permanent residence permit you can still be accepted for a loan if your spouse is a Japanese national or permanent resident and act as a joint guarantor.

Maximum loan: JPY 5 million to 300 million.

AU Jibun Bank is the banking branch of the second largest mobile carrier in Japan, AU. The bank has the lowest variable interest rates in the industry. Sadly, the English support is very limited.

Mortgage page: “Housing Loan” [JP]

Requirements: Permanent residency.

Maximum Loan: JPY 5 million to 200 million.

ARUHI is known for its market-leading fixed-rate interest loans and is relatively friendly to foreigners.

Mortgage page: "ARUHI Super Flat Fixed-Rate" [JP]

Requirements: Permanent residency or special permanent residency.

Maximum loan: JPY 1 million yen to 80 million.

Sony Bank is digital “NEO” bank with no physical locations. The bank is known for its ease of setting up an account as a foreign national due to its relaxed application process and English online platform. For home-loans, the bank does not offer English or special treatments to foreigners.

Mortgage page: "Home Loan"[JP]

Requirements: Permanent residency.

Maximum loan: JPY 500 million to 2 million.

| NEOBANK 住信SBIネット銀行")

SBI NEOBANK is a digital “NEO” bank with no physical locations. It is known for offering some of the cheapest variable-interest rates on home loans in the industry but is severely lacking in English support.

Mortgage page: "Net-only incapacity insurance housing loan"

Requirements: A bit unclear. At the time of application, a prescribed identity verification document with a status of residence is required.

Maximum loan: JPY 1 million to 100 million.

Rakuten Bank is Japan’s biggest digital “NEO” bank with no physical locations and is relatively friendly to foreigners. If you are a customer of Rakuten’s other services, such as Rakuten Credit card, Rakuten Mobile or Rakuten Securities, you can combine the services for discounts.

Mortgage page: "Variable interest rate (with fixed rider)"[JP]

Requirements: Permanent residency. However, sometimes residents with a "Special Permanent Resident Certificate", a "Residence Card" within the period of stay, or "Alien Registration Card [Zairyu card]" can be accepted.

Maximum loan: JPY 5 million to 100 million.

5. Best Japanese real-estate portal websites

The top 5 Real-Estate websites in Japan (ranked in order of popularity):

")

suumo.jp - Japan’s biggest real-estate site. Have the biggest selection of homes, both for purchasing and renting.

o-uccino.jp - Very similar to Suumo, but has a somewhat different library.

homes.co.jp - Biggest direct competitor to Suumo, with some more filtering features and the ability to sort houses via an interactive map.

athome.co.jp - Modern interface with interesting filtering features, such as for surfing spots or for warehousing

realestate.yahoo.co.jp - Barebone real-estate portal with few options. I do not understand why people use it

The most popular English real-estate website in Japan:

https://realestate.co.jp/ - English real-estate portal connected with English speaking real-estate agents listing foreigner friendly property owners. Recommended for people who are not familiar with the Japanese real-estate market.

6. Conclusion

Japanese home-loans are still ridiculously cheap and even though getting them are cumbersome, especially if you aren’t a permanent resident here, it is definitely possible.

On top of that, the Japanese housing market has fared quite well this year despite the global fall in home-prices.

If you would like to know more about investing in Japanese real-estate, and my thoughts on investing in it, be sure to check out this article: