Stock Analysis: EIZO (JP 6737) - Japan's Last Monitor Maker with an Incredible Turnaround Story

EIZO has done an incredible pivot from gambling monitors to becoming the gold standard for professionals. The question is, should you buy its stock?

Disclaimer: The information in this article represents my opinions and should not be construed as personalized or individualized investment advice and are subject to change.

You might not have heard of EIZO, but it's considered the gold standard in the professional monitor world.

If you work in digital design, healthcare, finance or the security industry, chances are that you or your company has paid multiple times the price of a regular monitor to get your hands on an EIZO screen.

With the demand for professional monitors increasing and a manufacturing renaissance in Japan, could EIZO be a great stock to invest in?

Overview

EIZO is the Japanese word for 'image' and is also the name of the most-respected high-end monitor manufacturer.

Since 1968, the brand has developed high-quality monitors and display solutions for use in gambling, finance, healthcare, the graphic industry, air-traffic control and shipping.

The company is one of the only monitor companies with a 100% in-house manufacturing and most of the manufacturing and quality control is performed in Japan.

An extremely agile company

EIZO has shown that it is capable to adapt to a quickly changing market. In fact, of all monitor manufacturers in Japan, once the world’s largest monitor producer, EIZO is the only one left standing.

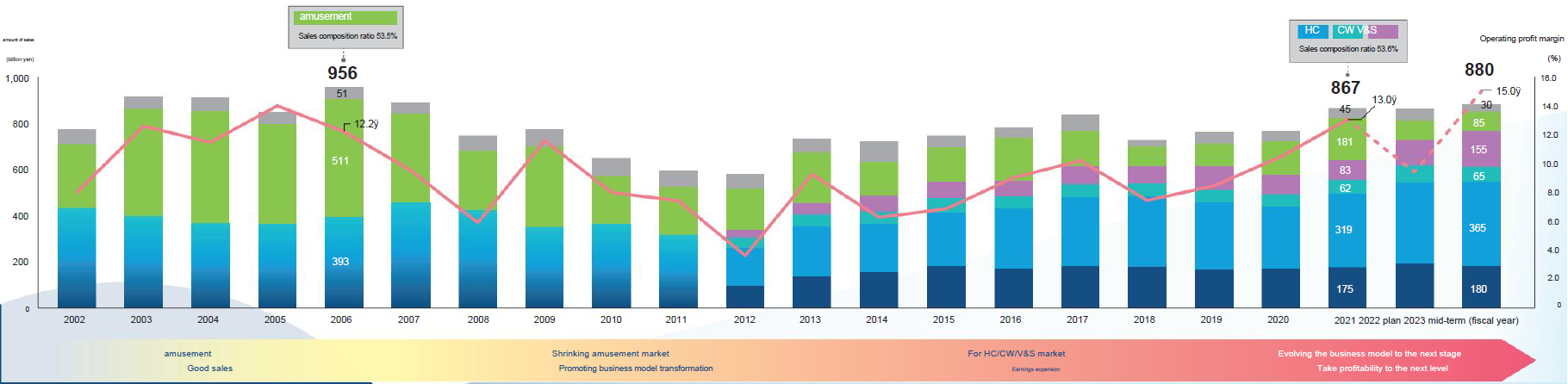

In 2006, EIZO shifted part of its structure away from its most profitable area, Amusement (Pachinko, or Japanese gambling machines), to high-end office monitors (B&P) and healthcare. Amusement stood for over 50% of all revenue in 2006, but now stands for less than 15%. Yet, revenue has largely recovered and since 2012 EIZO’s revenue has increased by more than 50%.

This is indeed a good sign that the company's leadership is well-equipped to deal with changing markets and new challenges.

Table of Content

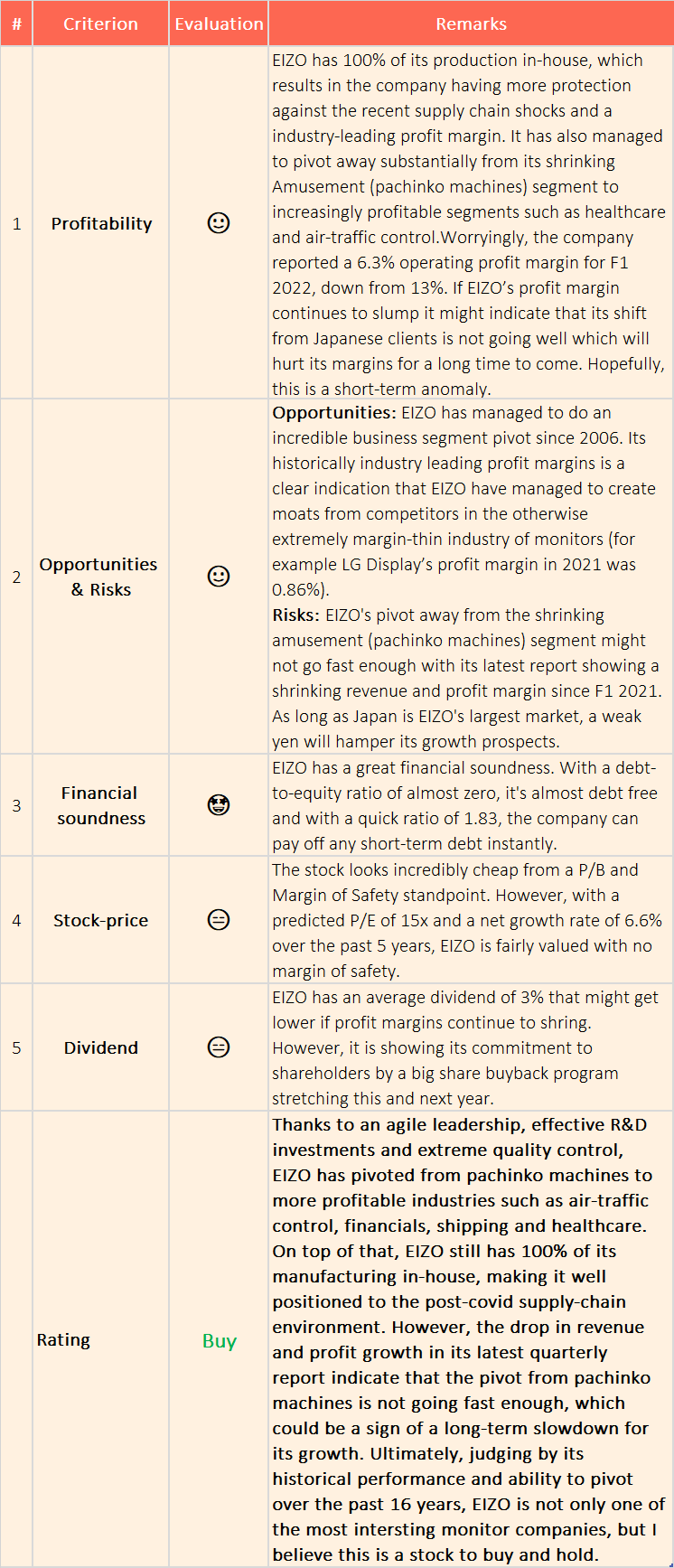

0. Konichi-Value Score

🤩 = Amazing

🙂 = Good

😑 = Acceptable

😖= Bad

1. Profitability

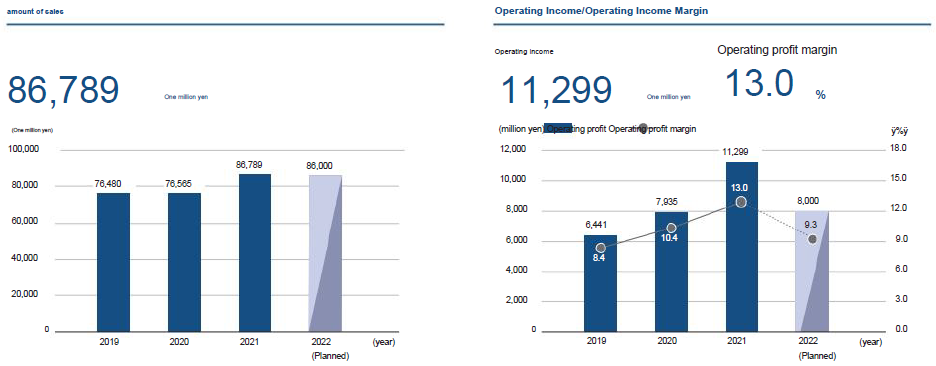

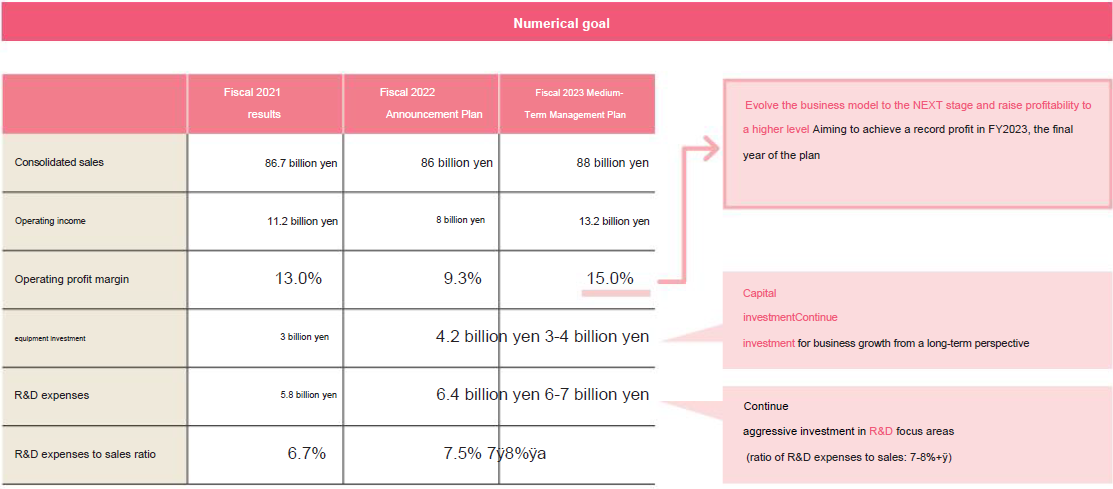

According to the latest financial report (Q3 2022), operating margins are hit substantially in all segments by supply-chain shortages, especially when it comes to semiconductors, a necessary component for all of EIZO’s products.

However, due to EIZO having a 100% of its production in-house, the company has managed to stave off the supply-chain shocks better than its competitors. However, even though its margin is better than most competitors, a projected fall in operating profit margin from 13% to 9.3% still has a big impact on its upcoming profits.

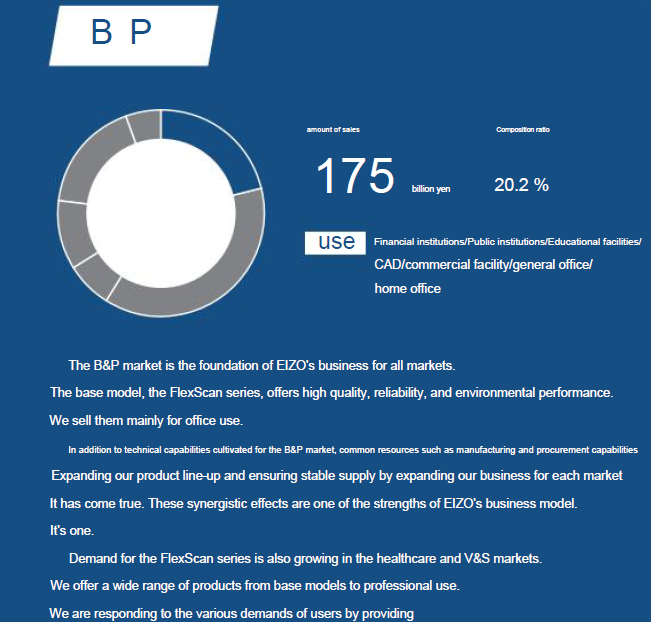

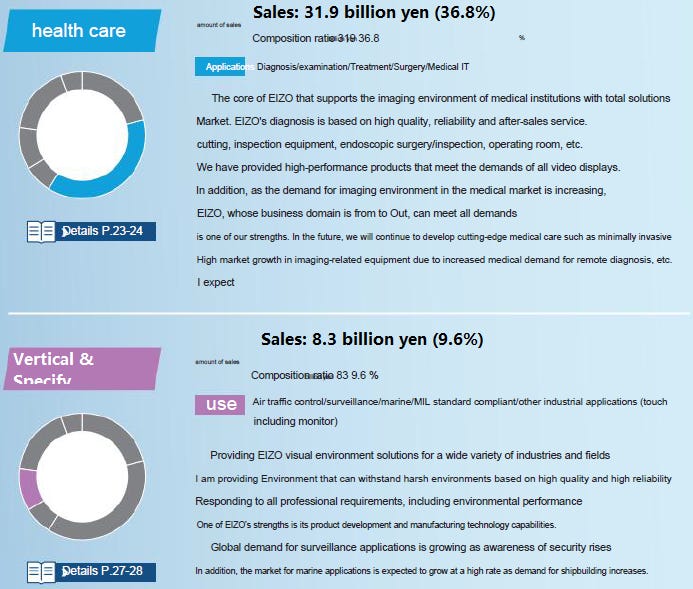

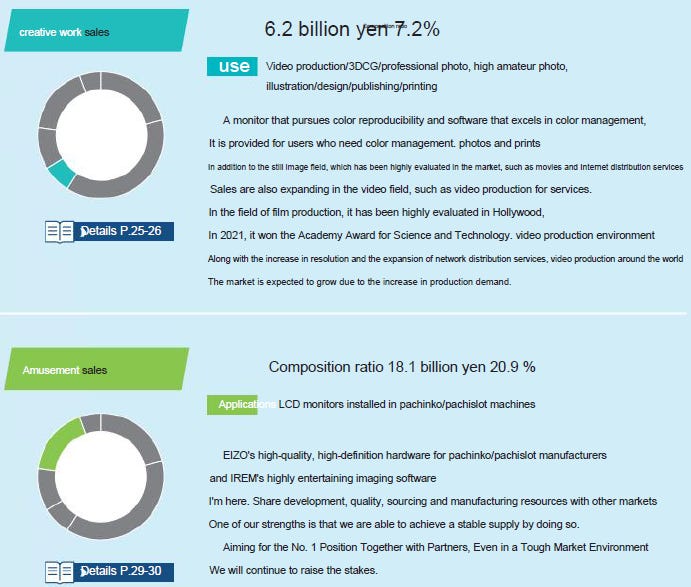

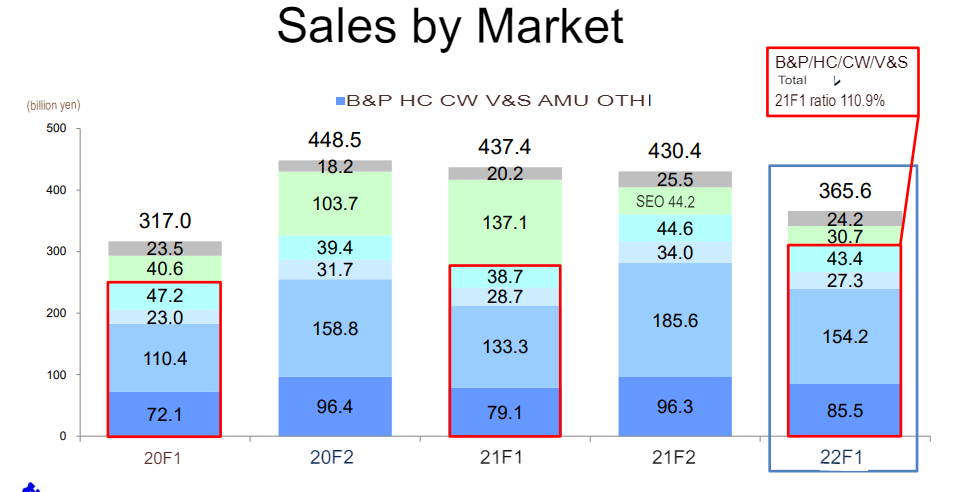

Below is the revenue size for each of EIZO’s main segments [machine translated from Japanese]:

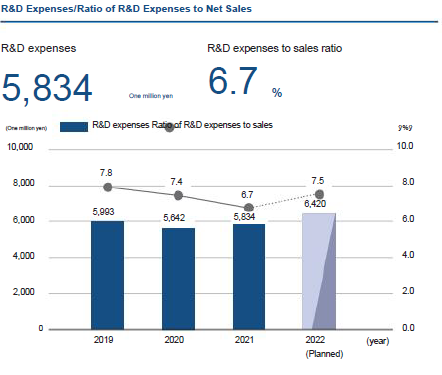

EIZO’s main segments are monitors for professional offices (BP) and Japanese Pachinko machines (Amusement) with around 41 of total revenue deriving from them. The company is quickly pivoting to more profitable markets, such as healthcare, air-traffic control and creative work, which is why the leadership is planning to increase its R&D spend:

Lastly, as EIZO hosts a 100% in-house manufacturing, it does have a heavy asset load on its balance sheet, which decreases its return on equity (ROE) and return on assets (ROA). However, the company has very high profit margins both historically and in the monitor industry:

As the manufacturing industry is increasingly emphasizing slack in supply chains and increased inhouse manufacturing, EIZO is already ahead and likely to be so for the foreseeable future.

Worrying Financials for First Half of Fiscal Year 2022

Worryingly, the company reported a 6.3% operating profit margin for F1 2022. According to EIZO, this is due to material procurement being done in USD, which has made it substantially more expensive than expected due to the sudden drop in the JPY. The reason this has had such a negative effect on EIZO’s profit margin is due to its main segment still being amusement, which solely has Japanese customers and hence payments in Japanese yen.

If EIZO’s profit margin continues to slump it might indicate that its shift from Japanese clients is not going well which will hurt its margins for a long time to come.

2. Opportunities & Risks

As previously mentioned, EIZO has managed to do an incredible pivot since 2006, shifting its main segment away from screens on amusement (pachinko machines) to high-end business screen, healthcare devices, air-traffic control shipping and other much more niche and specialized markets.

That EIZO has been able to break into these specialized markets successfully in such a short amount of time is impressive in itself, but that the company has managed to do this while reporting record operating margins of 13% in FY2021 (April 2021-March 2022) is astonishing.

This is a clear indication that EIZO have managed to create many moats from competitors in the otherwise extremely margin-thin industry of monitors (for example LG Display’s profit margin in 2021 was 0.86%).

![Economic Moat: Identify Warren Buffett Type Indian Stocks [2022] - GETMONEYRICH](https://substackcdn.com/image/fetch/$s_!irZe!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2F4ac6e19f-ab8f-4889-8a35-e49c1201717a_516x421.png "Economic Moat: Identify Warren Buffett Type Indian Stocks [2022] - GETMONEYRICH")

The leadership at EIZO are also sure that they have created a strong enough moat to continue increase the company’s revenue and profit margins as supply-chain shortages subside (FY2023):

Risks

As stated earlier, supply-chain shocks and decrease in demand will have substantial effects on EIZO’s bottom line.

For FY2023 (April 2022-March 2023), EIZO is just predicting that the upcoming recession will have a 0.9% decrease in its revenue. However, the supply-chain shocks are predicted to affect the company’s operating income margin from 13.0% to 9.3%.

Looking at previous financial reports, the EIZO leadership has shown to be conservative with their estimation, so if anything, we can expect these numbers to be relatively pessimistic.

However, perhaps the biggest risk is EIZO’s massive pivot away from Amusement (Japanese Pachinko machines) described in the “Opportunities” section. The company has definitely shown that its capable of breaking into niche markets, but not without costs:

From F1 2021 to F1 2022, revenue from Amusement has gone down by 78.1% while the increase in other segments is only 10.9%, which has resulted in a revenue decrease of JPY 71.8 billion.

EIZO has still delivered a positive net income growth rate of 6.6% annually for the past 5 years, but if all sectors except Amusement don’t grow faster, it might turn negative.

On top of that, the report also shows a decrease in profit margins to 6.3% from 13% same period last year. As explained in the previous section, this is due to the unforeseen strength in the USD, but as EIZO is a net-exporter, a weak yen should benefit the company. If the profit margin continues to stay in single digits, it is a worrying sign that EIZO is not able to pivot from its local and shrinking Amusement segment to global, more profitable clients fast enough.

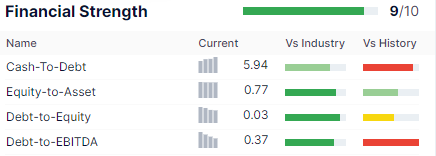

3. Financial soundness

As with most Japanese companies in manufacturing, EIZO has a great financial soundness. With a debt-to-equity ratio of almost zero, the company is almost debt free and with a quick ratio of 1.83, the company can pay off any short-term debt instantly.

4. Stock-price

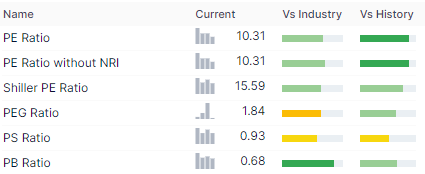

EIZO’s Price-to-Earnings (P/E) ratio with the predicted earnings for FY2022 is around 15x.

However, with the company’s FY2021 earnings, its P/E is as low as 10.31x:

More incredibly is that the stock also trades at a Price-to-Book (P/B) ratio of 0.68. That means that theoretically, if EIZO sold off all its assets today, shareholders would get 42% more money than they paid for the stock.

Such a P/B is incredibly low for a company that has developed and holds technologies and patents used for specialized industries like healthcare or air-traffic control. Likely, the market is yet to price in that EIZO has pivoted from a more general monitor manufacturer to a successful specialized one.

However, with a predicted P/E of 15x and a net growth rate of 6.6% over the past 5 years, its valuation looks relatively high. As the stock-market is trending downwards, let’s require a low rate of return of 5%. This gives us a P/E of 15x as a fair valuation for EIZO, which is right where the stock is expected to be by the end of the year.

However, as the company is going through a seemingly successful pivot, its growth and profit rate should pick up soon, but for now, I conclude that EIZO is fairly valued with no margin of safety.

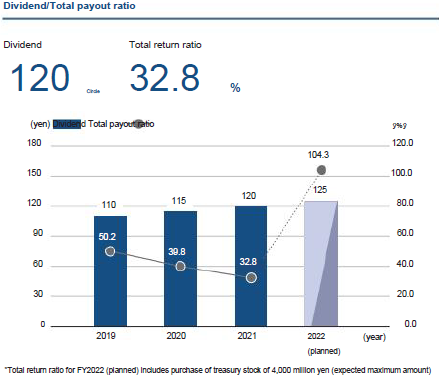

5. Dividend & Share buybacks

EIZO has an average dividend ratio of around 3%. It has moderately increased dividend for the past 5 year. However, as the company has a policy of pay out around 30% of its profits in dividend, it might go down if profit margins continue to be at the present 6.6% level.

EIZO recently announced a share-buyback plan that will purchase up to 3.52% of all shares issued. This is a big commitment for a Japanese company and indicates that the leadership believes that the company is healthy with good long-term prospects.

6. Conclusion

EIZO is an incredibly interesting monitor manufacturer. It is the only major monitor manufacturer left in Japan, a country that was once the biggest screen producer in the world. Thanks to an agile leadership, effective R&D investments and extreme quality control, the company has managed to pivot away from its local amusement segment (read: pachinko machines) to niche and more profitable industries with much bigger moats than general screens, such as air-traffic control, financials, shipping and healthcare.

On top of that, EIZO still has 100% of its manufacturing in-house, a practice that was often seen as negative when lean production and just-in-time logistics were the practices to strive for. However, with the recent pandemic resulting in companies realizing the importance of slack in supply chains and China being seen as a less reliable manufacturing hub; EIZO is positioned to take full advantage of this new environment.

Nonetheless, the drop in both revenue and profit growth in EIZO’s latest quarterly report indicate that its pivot from the Japanese amusement segment is not going fast enough, which if sustained, could be a sign of a long-term slowdown for EIZO’s growth.

Hopefully this is just a short-term anomaly in the otherwise successful pivot history of EIZO. Therefore, I would definitely strongly recommend that you wait for EIZO’s next quarterly report before making any major investments in its stock.

Ultimately, judging by the company’s historical performance and ability to pivot over the past couple of years, EIZO is not only one of the most intersting monitor companies in the world, but I believe this is a stock to buy and hold.