[Stock-Analysis] MUJI (Ryohin Keikaku): Japan's Most Famous Furniture Brand Punching Below its Weight

Muji, with its parent company Ryohin Keikaku, is still lagging behinds its peers Uniqlo and Nitori, but that might make the stock more interesting to value-investors.

Disclaimer: The information in this article represents my opinions and should not be construed as personalized or individualized investment advice and are subject to change.

*This analysis was updated 2022/11/18 with new information regarding its rating

*This analysis’ data is mainly based on Muji’s financial report from FY2022 (April 2021-March 2022)

Previously, I wrote about the less known but recently more successful home-furnishing company Nitori (check out that article here). So, I thought it would only be fitting to take on the older brother of Japanese home furnishing, Muji!

Muji, or Mujirushi Ryohin (translates as “no-brand, quality goods”) as it is known in Japan, is perhaps the world’s most famous Japanese home-furnishing brand.

Muji began as a product brand of the supermarket chain The Seiyu, Ltd. in December 1980. The Mujirushi Ryōhin product range was developed to offer affordable quality products and were marketed using the slogan “Lower priced for a reason.”

Ever since its inception, Muji has carved out a distinctive design language, which is extended throughout its more than 7,000 products. Commentators have described Muji's design style as having mundanity, being "no-frills", being "minimalist", and "Bauhaus-style".

Muji product design, and brand identity, is based around the selection of materials, streamlined manufacturing processes, and minimal packaging. Muji products have a limited color range and are displayed on shelves with minimal packaging, displaying only functional product information and a price tag.

This has helped Muji differentiate itself and today the company’s products are often sold at a premium to competitors like IKEA and Nitori.

Konichi-Value Score

🤩 = Perfect

🙂 = Good

😑 = Acceptable

😖 = Bad

Table of Content

1. Profitability

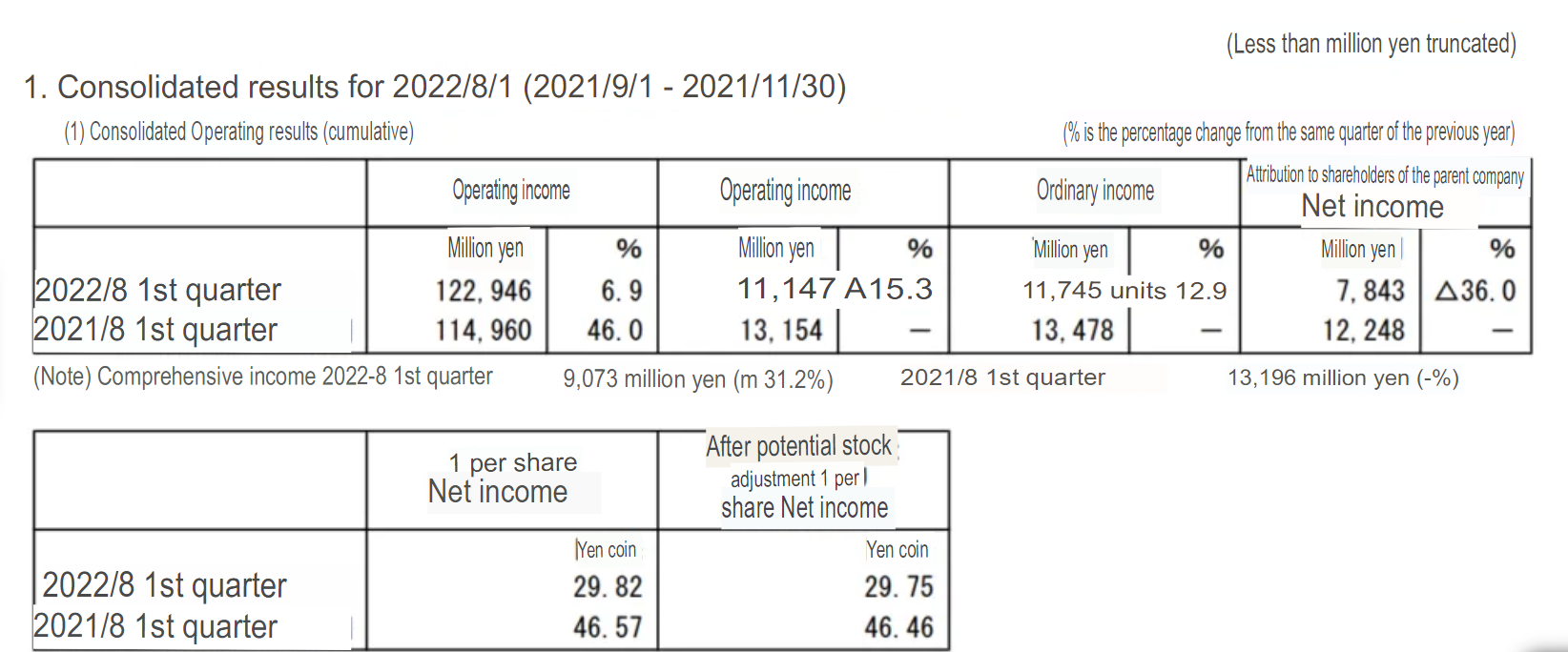

This is a summary of financial results for the first quarter of the fiscal year ending August 31, 2022.

Net sales for the first quarter of the current fiscal year were ¥122.9 billion, up 6.9% year-on-year. Operating income decreased by 15.3% to ¥11.1 billion. Net income (EPS) per share was ¥29.8 million.

The sales have reached an all-time high. According to Muji’s financial report, this is due to the increase in the number of stores in Japan and overseas.

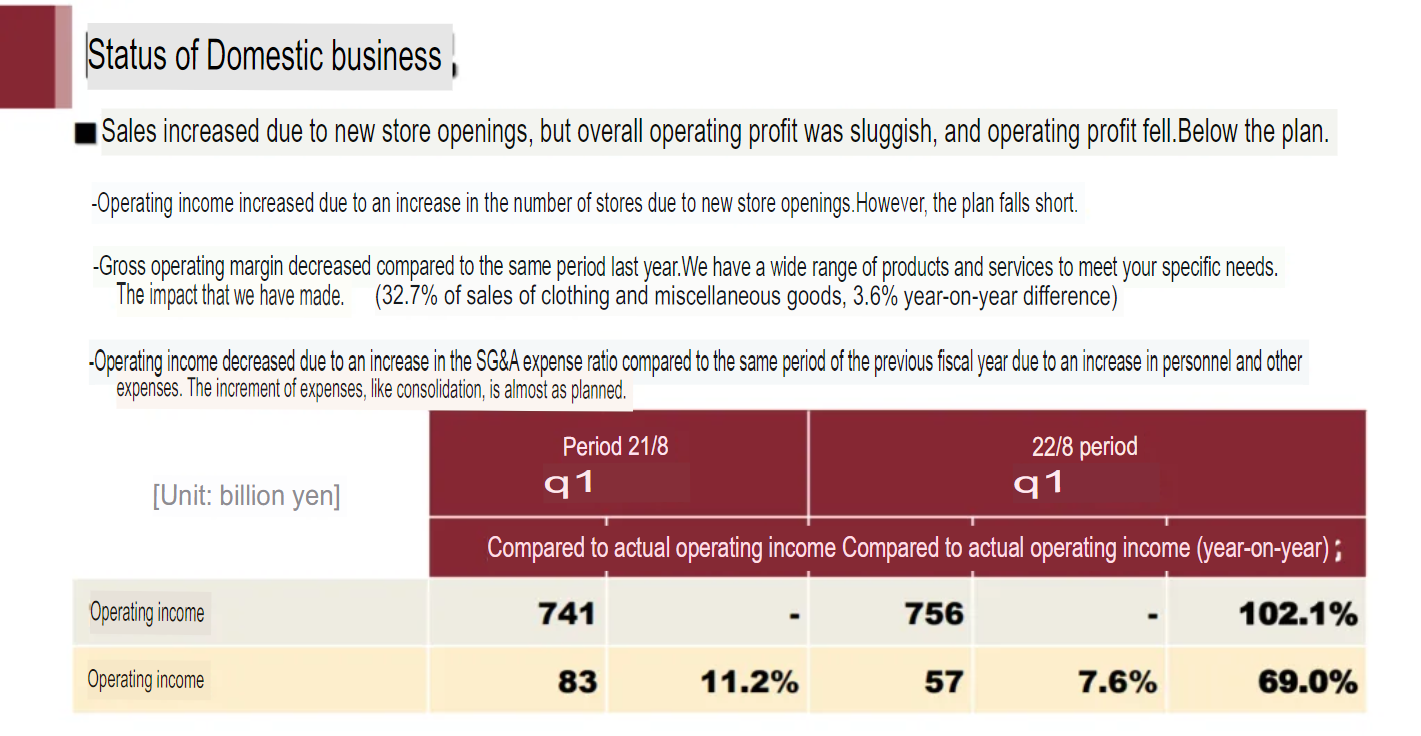

Domestic business

Muji has been increasing its expansion even during the Covid-19 pandemic. Due to new store openings, net sales increased by 2.1% compared to the same period last year, but operating income decreased by 31%.

This is due to the fact that sales of clothing and miscellaneous goods have declined significantly from the plan.

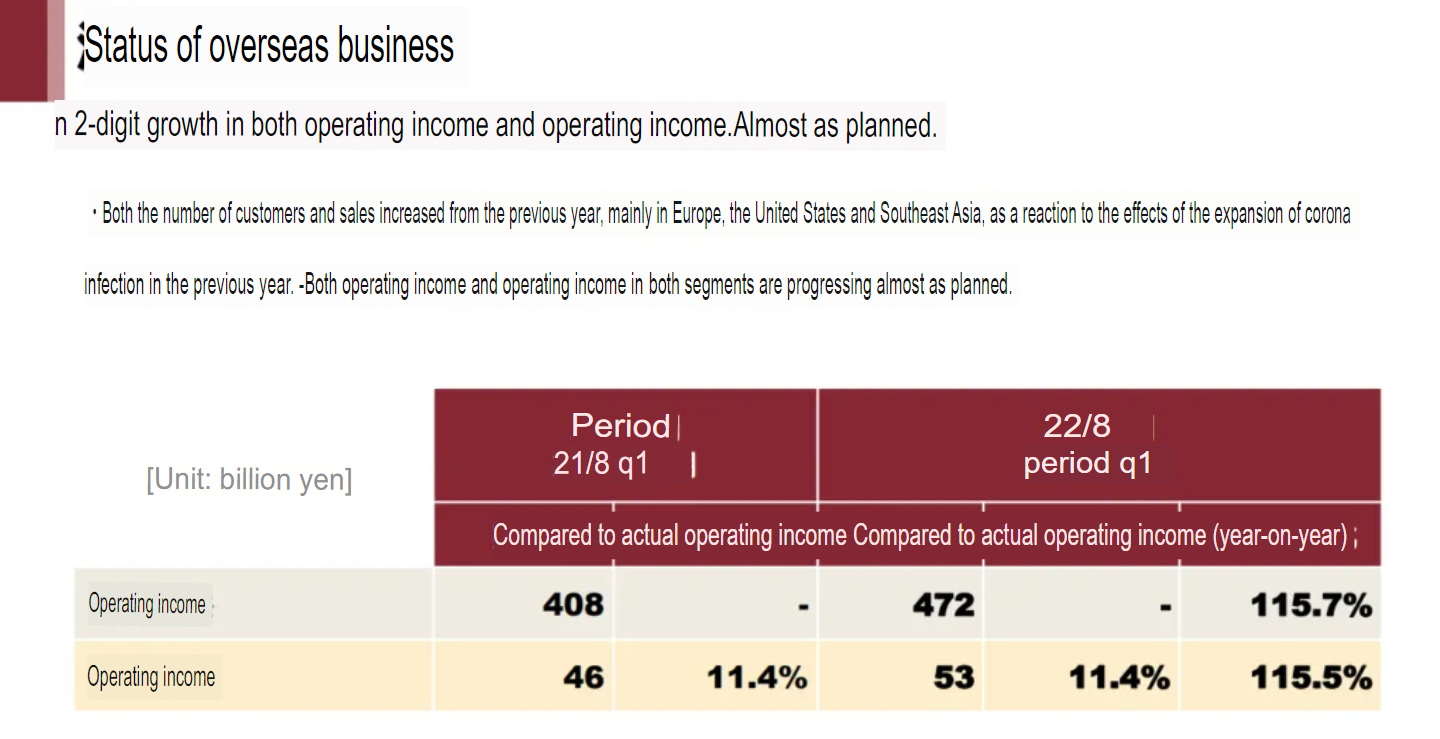

Overseas business

Both operating revenue and operating income grew by around 15%. Last year's overseas business struggled mainly in Europe due to the impact of Covid-19, and hence the numbers that had to be beaten in Q1 were relatively low.

In China, which accounts for the majority of Muji’s overseas business, 13 additional stores were opened from the end of the previous fiscal year, but as with Japan, Muji is struggling with sales of clothing and miscellaneous goods, and total sales were therefore flat.

2. Opportunities and Risks

Opportunities

Muji is one of the most recognized Japanese brands, and it’s mostly due to their successful overseas expansion. In September 2021, the company managed to open its 1000th store and it’s spending massively on new stores abroad. As the Japanese market is saturated and overseas tourism is likely not coming back to pre-pandemic levels any time soon, Muji has an up compared to other Japanese home-furnishing companies as they can easily leverage their brand in growing markets, especially mainland China and Southeast Asia.

As homeownership and the demand for high-quality Japanese furniture has shown exponential growth in these markets, Muji is the perfect brand to ride on this wave without much marketing effort. Muji’s leadership has also shown that expanding to east Asia has generated much higher profits than Europe and the US.

Risks

China is Muji’s fastest growing market, which brings two problems: The first one was highlighted with the use of Xinjiang cotton sourcing which the company downplayed as an issue earlier this year, whilst some other Western brands were more forthcoming in criticizing Chinese authorities. This could have an adverse effect in some markets.

The second issue is the company's growing reliance on China, as longer term it will probably become its biggest market. 'MUJI' may be seen as onside with the Chinese authorities currently, but geopolitical tensions can flare up and consumer behavior can be affected dramatically (although these cases tend to be temporary). China brings commercial opportunity but also fairly large risks, something that other regions do not come saddled with. In this context I would prefer to see the company make more efforts to grow in countries such as Indonesia (only 6 stores) and Vietnam (no stores currently) where there may be different challenges but not a growing risk profile.

However, the main risk I see is imitation in Muji’s products. Barriers to entry for minimalist 'MUJI'-like products are low, as seen by products by Uniqlo (OTCPK: FRCOY), Daiso Industries (private) and China's Miniso (MNSO). The company must continually innovate and compete versus discount stores.

3. Financial soundness

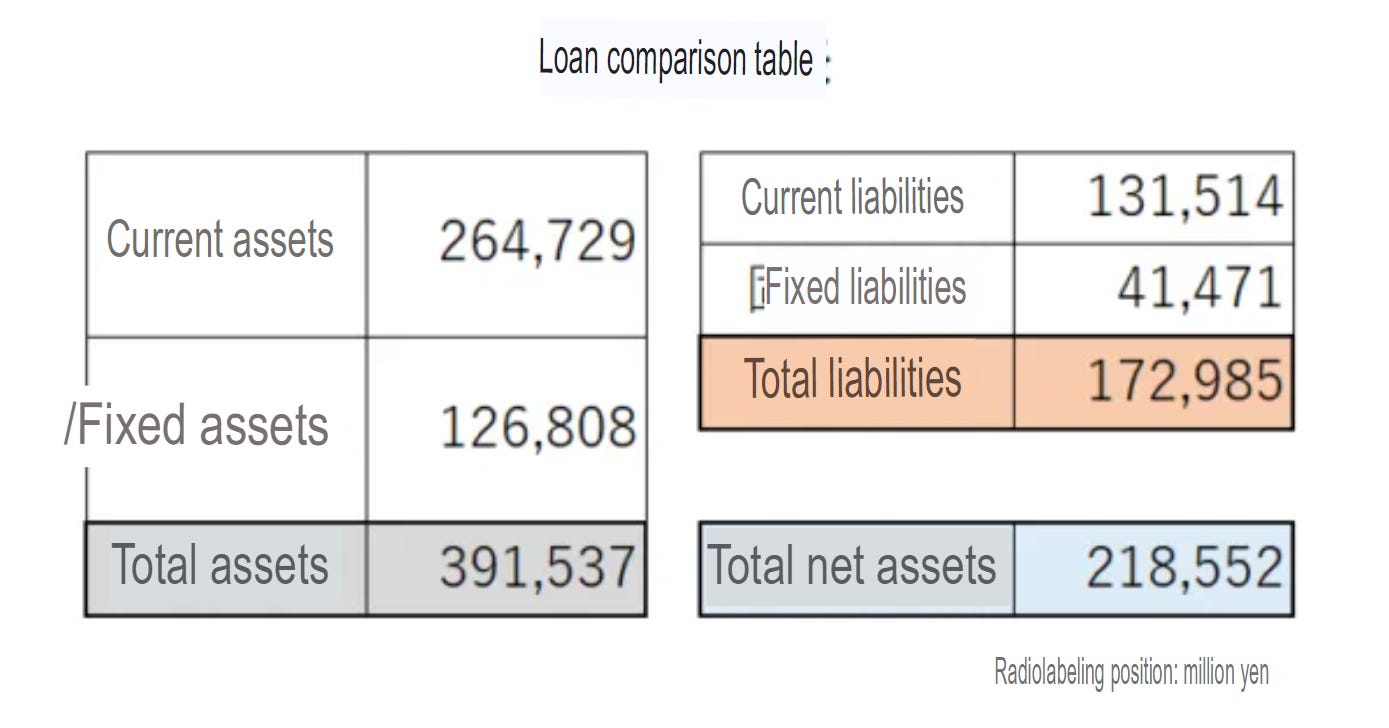

Next, let's look at Muji’s financial situation. First, the breakdown of assets.

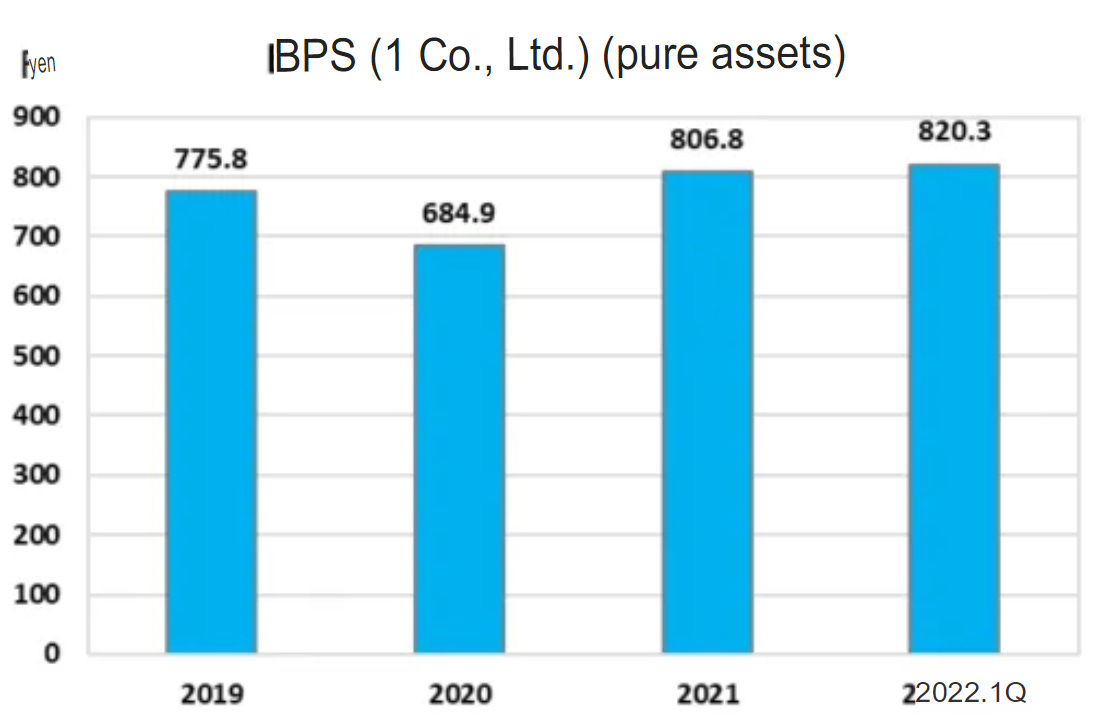

Total assets were 391.5 billion yen, of which liabilities were 172.9 billion yen. The capital adequacy ratio is 55.1%.

Net assets (BPS - Basis Points) per share are ¥820.3. As the graph shows, in the last three years, there has been no significant change in BPS.

Considering how exposed Muji has been to the effects of Covid-19, this is impressive to say the least.

To summarize, a Capital Adequacy Ratio of over 50% is strong enough to not worry any investor of default risks. On top of that, that Muji has been able to hold a stable net asset ratio over the pandemic while expanding is very impressive.

4. Stock-price

The stock price is 1,268 yen as of July 8th, 2022.

The stock has been on a continuous downtrend from 2,480 yen on July 8th, 2021. That is a 49% drop since its peak despite record sales!

However, Muji has been very highly valued for a long time with an average Price-to-Earnings ratio (P/E) of 20 over the past 10 years. Its P/E ratio has come down to 13.52.

As China is the company’s biggest market, I am worried that we will see a big loss of revenue in the coming quarters which will increase its P/E substantially. Therefore, even though I believe Muji is undervalued at its current P/E-ratio, I think there is a big risk it will go up soon.

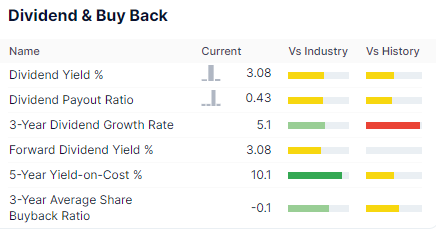

5. Dividend

The dividend yield for Muji is OK, but considering the company is in a growth phase, I believe it is definitely more than good.

6. Conclusion

At the current share price, I do not want to buy shares of Muji (Ryohin Keikaku).

The reasons are as follows:

Results

Looking at the current situation, it is difficult to predict the future where profits will grow significantly. In particular, clothing sales are struggling not only in Japan but also in other countries, and although the number of stores has increased, sales and profits have not increased as expected.

If Muji can follow in the footsteps of Nitori, I can see it growing substantially in South-east Asia and Europe, but as of now, this is just hopeful thinking.

Financial status

Muji’s earnings growth has not increased steadily over the past three years.

It seems that the Covid-pandemic has affected this, but it is still not a good sign.

Stock price index

If you look at the stock price from the P/E perspective, it looks like the stock is cheap historically, and if you look at it from the P/B ratio, the stock is expensive.

In addition, the credit multiple is at a high level, and there is a possibility that there will be a lot of selling when the stock price rises. However, since the dividend is stable and the stock has brand power, I still believe that the stock is cheap long-term.

I've said a lot of negative things so far, but I think it has the potential to become a retailer with a global presence, like Fast Retailing (Uniqlo/GU) and Nitori HD. If its growth rate picks up, I would definitely justify its current P/E of around 16x due to the enormous potential the company has abroad.

MUJI's strength lies in its wide range of hit products (food, sweets, cosmetics, stationery, interior goods) and global brand recognition. If the company can continue to release hit products in the future, it will lead to further increases in corporate value.

However, I would not buy the stock currently…

Really love Muji for my entire life, but I’m dismayed to find it’s repeated failure in entering the US market (and Europe broadly). Western customers rave about the stationery, but not the furniture or the apparel (which do very well in China). That is something worth thinking about.

Thanks for this one. I’ve been in Ryohin Keikaku for the last few months now. I really like the risk/reward here, but I’ll admit i didn’t expect the yen to slide quite this hard. That has to be creating some extra challenges for them.

I’ve also been enjoying your last few posts as well. I especially liked the shimano one as it is just not one that gets much attention. Keep it up!