Please note: This article is for informational purposes only and is not intended as investment advice. The mention of specific stocks is not a recommendation to buy or sell any securities.

You are reading this because you looked at Nintendo’s stock chart recently and felt your stomach drop into your shoes. The stock has been tumbling in early 2026, plummeting nearly 40% year-to-date to close at an ugly ¥7,667 following the latest earnings report. And now it’s down another 8% since then!

Naturally, you might assume the big, bad hedge funds are shorting it into oblivion.

In fact, the short interest ratio is practically non-existent. The short interest volume actually plummeted by 43.5% in March. Borrow rates for short sellers are hovering between a measly 1.01% and 4.08%. If hedge funds were aggressively betting against Mario, those borrow fees would be skyrocketing.

So, if the shorts are not killing Nintendo, what is?

First, Switch 2 hardware momentum is sluggish. Sales hit 2.49 million units in the March quarter, causing Wall Street to sweat. Second, memory component costs and tariffs are squeezing the company, prompting Nintendo to officially forecast a 100 billion JPY hit to their cost of goods sold. Finally, Wall Street is terrified of a Google AI model called Genie 3 that supposedly makes game developers obsolete.

But is the market right, or are we seeing the greatest Nintendo undervaluation of the century?

Below, I analyze every bear case driving this sell-off to assess the stock's current investment potential:

The Fake Bear Cases:

Nintendo Switch 2 is a bust?

Currently, the narrative is turning sour because of the Switch 2 transition. The original Switch is long in the tooth. Sales are naturally declining.

The Switch 2 has launched, but the early sales figures are not meeting the hyper-optimistic Wall Street expectations. The company cut their production target from 6 million to 4 million units for the quarter. This caused weak-handed retail investors to panic and sell.

Adding fuel to the fire is Google DeepMind’s Project Genie 3. This AI model can supposedly generate playable video game worlds from simple text prompts in real-time. Tech journalists are screaming that the 200 billion USD gaming industry is dead.

Gaming stocks plunged as a result. Unity software dropped 35%. Nintendo caught the contagion and saw its stock drop 4.75% in a single session.

It’s a weird feeling of deja-vu when I hear this… People claimed mobile games would kill console gaming a decade ago. Nintendo responded by releasing the Switch and selling over 140 million units.

The current panic over the Switch 2 transition is entirely predictable. Every single time Nintendo launches a new console, analysts predict doom. They did it with the DS, they did it with the Wii, and they did it with the original Switch.

AI will make Nintendo obsolete

")

This is the most widely discussed risk, and it is also the stupidest. In January 2026, Google DeepMind released Project Genie 3. The market completely lost its mind over a tech demo.

The Tech: Genie 3 generates real-time, navigable 3D environments from text or image prompts.

The Specs: It outputs at 720p resolution and 24 frames per second.

The Features: It allows basic interactive physics, like jumping and swimming.

Why pay hundreds of developers for five years to build a Zelda game when an AI can generate one in five seconds? Gaming stocks nose-dived across the board.

Unity dropped 35% in a single day. Analysts downgraded the entire sector, claiming high-fidelity interactive content generation would erode the AAA studio moat. Even major Korean publishers like NCSoft had to release statements defending their business models.

Let me explain why this is pure, unadulterated garbage. Genie 3 generates visual environments, not video games. A video game is not just a landscape you walk around in aimlessly.

A Nintendo game is defined by meticulous, obsessively tuned gameplay loops. It is the exact friction of Mario’s jump. It is the perfectly balanced level design of a Mario Kart track.

An AI hallucinating a pixelated forest cannot replicate the intentionality of Shigeru Miyamoto’s level design. Genie 3 struggles heavily with multi-agent scenarios and lacks full gameplay features. It is a prototyping tool, not a game engine replacement.

Furthermore, Nintendo sells characters, not pixels. People do not want to play “Generic AI Platformer 7.” They want to play as Mario.

AI cannot generate copyrighted intellectual property without facing a nuclear lawsuit from Nintendo’s legal team. The market is conflating the automation of background asset generation with the obsolescence of creative game design. It is a fundamental misunderstanding of the industry.

Competition is killing Nintendo?

Let us compare Nintendo directly to its closest peers. Look at Sony Group Corporation (6758.T). Sony is an incredible company, but their gaming strategy is fundamentally different from Nintendo’s.

Sony focuses heavily on the hardcore, premium audience. They build massive, hyper-expensive machines like the PlayStation 5 Pro. They rely on bleeding-edge graphics to sell their products.

This is a dangerous game. It requires massive capital expenditures. It also puts them in direct competition with high-end PC gaming and Microsoft’s Xbox.

Sony’s financial metrics actually reflect a highly successful, albeit different, strategy. Following the spin-off of Sony Financial Group in October 2025, their balance sheet is pristine. They sit on roughly 2.09 trillion JPY in cash against 1.03 trillion JPY in debt, operating with a robust net cash position.

Their Game and Network Services division is also massively profitable. It pulled in a record 140.8 billion JPY in operating income during Q3 FY2025. However, Sony remains a massive conglomerate relying heavily on third-party software and bleeding-edge hardware.

Nintendo does not play this game. They focus on the mass market and casual gamers. You do not buy a Nintendo console for the graphics.

You buy a Nintendo console because it is the only legal way on earth to play Mario, Zelda, and Pokemon. That is the moat. Their intellectual property is impenetrable.

You can have all the processing power in the world, but if your kid wants to play Mario Kart, you are buying a Nintendo. This gives them incredible pricing power. Nintendo rarely discounts their first-party games, even years after release.

Furthermore, Nintendo is actively expanding beyond video games. They are finally monetizing their IP in the broader entertainment world. They launched The Super Mario Galaxy Movie globally on April 1, 2026, and it generated a staggering worldwide box-office gross of over $800 million USD in its first four weeks. They also have a live-action Legend of Zelda movie slated for May 2027.

This creates a self-sustaining flywheel. You watch the Mario movie. You buy the Mario game.

You visit the Super Nintendo World theme park. You buy the plush toy. Every piece of media feeds into the core software business.

Competitors simply cannot replicate this. Microsoft can buy Activision Blizzard for 69 billion USD, but they cannot buy cultural relevance. Master Chief does not sell theme park tickets like Mario does.

You might argue that Microsoft bought cultural relevance when they acquired Minecraft. You are completely right that Minecraft is a global phenomenon. However, Microsoft never figured out how to connect Minecraft to them, because there is no synergy between them and Minecraft.

So you end up with even Nintendo’s richest competitor failing to become a threat. Master Chief does not sell theme park tickets, and Steve from Minecraft does not force anyone to buy an Xbox.

This is the ultimate competitive advantage.

Nintendo’s finances are weak?

At first sight, this sounds absurd. In the fiscal year ended March 2026, Nintendo’s net sales absolutely exploded by 98.6% year-over-year to 2,313.0 billion JPY. Operating profit jumped 27.5% to 360.1 billion JPY.

However, Wall Street fixated on the profitability ratios. Because hardware made up a massive 66.7% of sales, Nintendo’s gross profit ratio cratered from 61.0% down to 39.3%. Operating profit margins also compressed severely from 24.3% down to 15.6%.

But look at the balance sheet. Nintendo is sitting on a war chest of 1,791.8 billion JPY in cash and deposits. They completed a share buyback in March 2026, acquiring and canceling 11.43 million treasury shares for 99.9 billion JPY. While this is a drop in the bucket compared to their total reserves, this massive cash position puts a hard floor on the stock price.

The Genuine Threats:

Too expensive to make the Switch 2?

This is the most legitimate threat to Nintendo’s short-term profitability. The bill of materials for the Switch 2 is skyrocketing. It is a genuine headache for management.

DRAM Costs: The 12GB LPDDR5X modules used in the Switch 2 have seen a massive 41% price increase this quarter.

NAND Costs: The 256GB NAND flash storage has risen by roughly 8%.

The bill of materials for the Switch 2 is skyrocketing. Nintendo officially warned that rising component prices, particularly for memory, and US tariff measures will slap an approximate 100.0 billion JPY impact onto their cost of goods sold for the coming year. Morgan Stanley analysts actually believe this 100 billion JPY estimate is too conservative given the expected surge in DRAM and NAND pricing.

Nintendo’s entire hardware philosophy relies on using cheap, commoditized components. This sudden spike in memory pricing destroys their hardware margins. They are used to making a profit on day one, not taking a loss like Sony or Microsoft.

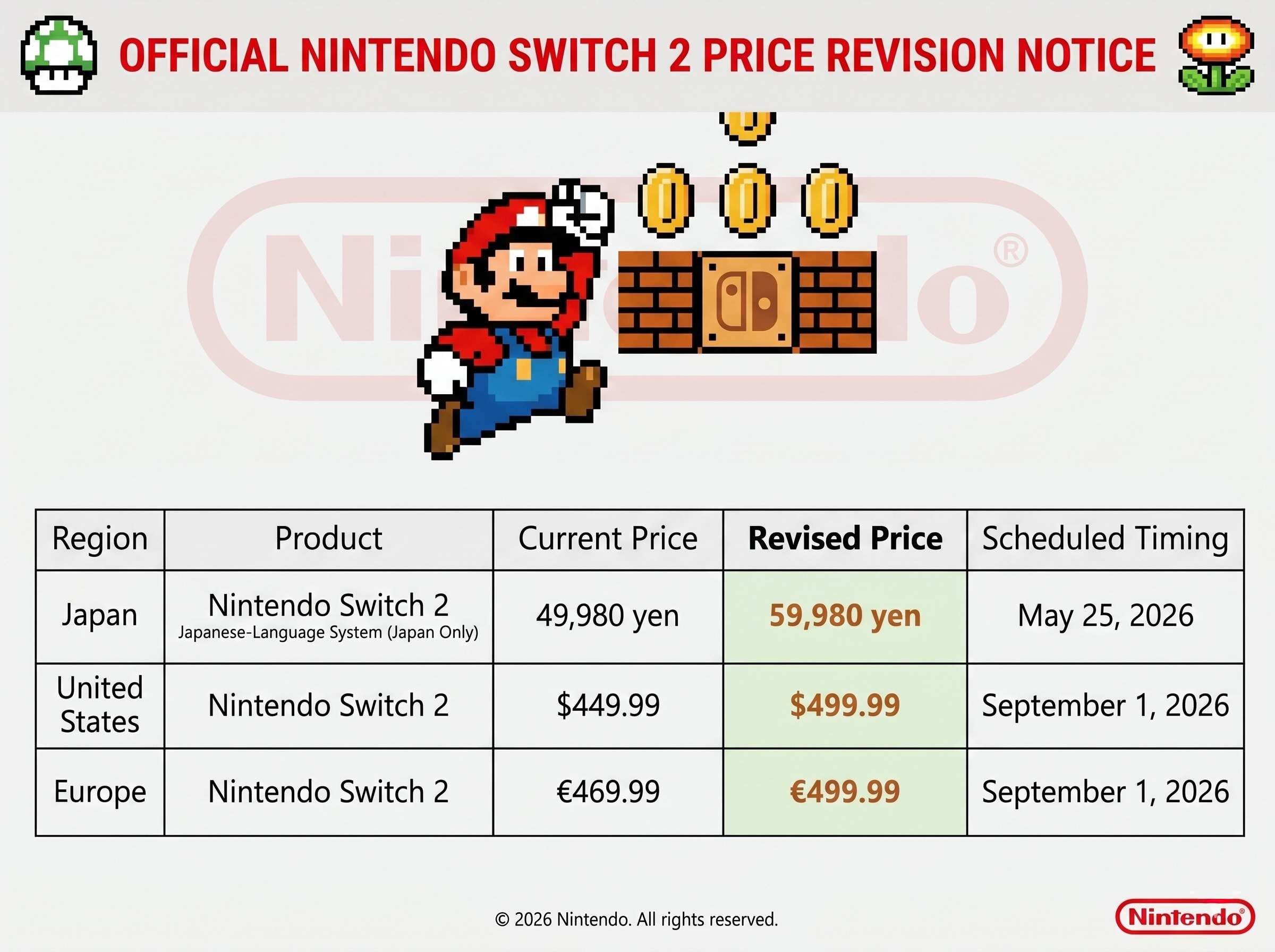

And they are sticking to that strategy. They are raising prices:

This is a risky move. Morgan Stanley warned that this price increase, combined with already sluggish Q4 momentum, warrants a cautious view on the pace of Switch 2 adoption. Raising prices mid-launch-window alienates the core casual audience.

Sure, this might slow down Switch 2 adoption, but this is still the cheapest console you can buy.

No good games?

The Switch 2 needs killer games to move hardware. Right now, the visibility is incredibly murky.

Pokemon Pokopia: Estimated 3.5 million shipments in Q4, performing well but needs to hold momentum.

Mario Kart World: Rapid shipment deceleration, with UBS predicting only 1.5 million shipments in Q4.

Upcoming Exclusives: Pokemon Winds & Waves is not slated until 2027.

If Nintendo does not announce a massive lineup of first-party titles soon, hardware sales will stagnate. Investors are desperately waiting for the next Nintendo Direct presentation. They need to see titles like the new 3D Mario or the rumored Fire Emblem: Fortune’s Weave.

Sure, they now have Yoshi and the Mysterious Book slated for May 2026 , Star Fox arriving in June 2026 , and Splatoon Raiders scheduled for July 2026. But again, none of these titles are enough to truly make the Switch 2 a must have console.

A weak pipeline is the fastest way to kill a console launch. The Wii U failed largely because of software droughts. If Nintendo repeats that mistake, the stock will bleed further.

Conclusion: Buying the Panic

In this analysis, I have established that the short sellers are practically non-existent. I have also established that Google’s Genie 3 is a hallucinating prototype, not a replacement for creative game design. The true headwinds are entirely cyclical, stemming from elevated RAM costs and the bold, risky decision to jack up the retail price of the Switch 2 to protect margins.

Wall Street is notorious for punishing cyclical transition years in the hardware business. They are completely ignoring the fact that a massive portion of Nintendo’s market capitalization is just cash sitting in a vault.

When you back out the 1,791.8 billion JPY in cash and deposits, you are buying the core operating business at a steep discount. You are buying a premier entertainment monopoly that owns the childhoods of multiple generations. You are paying a discounted multiple for Mario, Zelda, and a business model that captures margin at every single step.

This is the essence of value investing. You buy a phenomenal business when temporary friction causes weak-handed investors to panic. The margin of safety is built entirely on that cash pile and the unbreakable strength of their intellectual property.

I do not care if memory prices force retail price hikes and compress adoption for a quarter or two. I care about the recurring software revenue and console adoption over the next decade. Buy the dip, collect the 219 yen dividend, and wait for the market to wake up to reality.

Well done, Rei! I like setups like this very much. RAM will not stay that expensive forever….this place is safe to wait it out. As you said, the company can survive years without cashflows….

Thanks for the article. Nintendo core customer cohort analysis is worth a look. If there is a structural concern, it’s here I suspect.