[Stock-Analysis] muRata Manufacturing: Parts-Provider to Apple & Likely Winner of the Manufacturing Boom in Japan

Disclaimer: The information in this article represents my opinions and should not be construed as individualized investment advice, and are subject to change.

All the stars are aligned for Japan to once again reclaim the title as a manufacturing powerhouse: The country is the most politically stable country in Asia, Japanese salaries have stayed basically stagnant since 1992 and the Japanese yen has lost almost 40% in value to the US-dollar in less than a year. All this is happening while companies are fleeing the from the world’s largest manufacturer, China, due to political turmoil, Covid-lockdowns and rapidly increasing salaries.

One company that looks to truly benefit from this trend is Murata Manufacturing, one of the world leaders in electronic component manufacturing:

Overview

Murata Manufacturing (6981 JP) manufactures and sells electronic components for electronic devices such as smartphones, PCs, and automobiles. The company’s main products are capacitors (see description in image below) and but it also provide components such as inductor coils and filters. Many of its products have global reach, and are crucial to most smartphones, especially the Apple iPhone, but also to cars, IoT products and wearables.

Murata is exceedingly reliant on global sales with overseas sales ratio exceeds 90%. As of the end of March 2022, the company is developing its business with a wide network of 29 domestic affiliates and 60 overseas companies.

By application, telecommunications accounts for 43% of sales and mobility accounted for 18.6%. In terms of sales by region, Greater China accounts for 54.8% (down from 58.4% in 2020), and it seems that the ratio is increasing because Apple owns a factory in China. Attention should also be paid to developments in China and Murata is very aware of its risks. In fact, they have cancelled some new factory build-outs in China in favor of focusing on its Japanese manufacturing arm.

Konichi-Value Score

🤩 = Amazing

🙂 = Good

😑 = Acceptable

😖= Bad

Table of Content

Profitability

Opportunities and Risks

Financial soundness

Stock-price

Dividends & Share-buybacks

Conclusion

1. Profitability

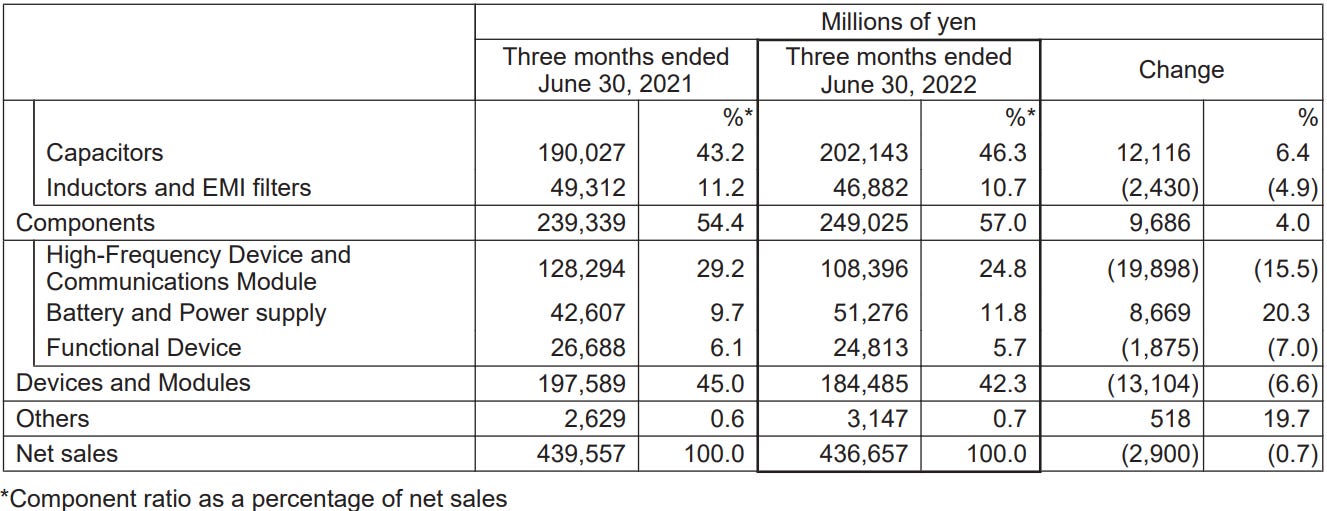

Review the financial results for the first quarter of the fiscal year ending March 31, 2023:

Net sales were 436.7 billion yen (-0.7% YoY) while operating income went down to 88.6 billion yen (-15.7% YoY). Income before income taxes reached 101.2 billion yen (-2.4% YoY). Net income per share was at 118 yen (-2.2% YoY).

In the overall electronics market, demand for parts has declined due to the impact of the lockdown in China and prolonged semiconductor & other specialized component shortages, resulting in a decline in production volume of smartphones, PCs, automobiles, and other products. Hence, the downturn for Murata can be seen more as a supply shortage than a demand shortage.

Sales of capacitors increased by 6.4% year-on-year due in part to an increase in sales of base stations and wearable terminals, as well as the impact of exchange rate fluctuations due to the depreciation of the yen. In the high-frequency and telecommunications segments, due to a decrease in the number of smartphones produced, there was a significant decrease of net sales by 15.5% year-on-year.

Orders received in the first quarter, with the exception of the Battery & Power supply division, were all below the prior-year quarter, a total decline of 14%. The leadership explains that the main reasons are the lockdown in China and the lower in demand for smartphones and PCs after its peak during 2020-2021.

Orders received in the first quarter, with the exception of the Battery & Power division, were all below the prior-year quarter, with a total decline of 14%. It seems to have been affected by the lockdown in China and the decline in demand for smartphones and PCs.

In summary, this fiscal year, the situation is expected to be severe, partly due to the rise in U.S. interest rates and of global economic slowdown.

Sales

Sales are on an upward trend. The impact of the increase in sales of mainstay capacitor products is large.

Operating Profit and Operating Margin

EPS (Net Income Per share)

Operating income and EPS are also on an upward trend. The operating margin is around 22%, which is a very high profit structure.

The weakened yen, which now approaches 150 yen to a US dollar, is also helping prop up the company’s bottom line as 65% of its production is done in Japan but more than 90% of sales are made overseas.

Compared to competition

Compared to competitors, especially Murata’s main peers General Packer (6267 JP) and Omron (6645 JP), its profit margins and Return on Equity are outstanding!

That Murata is losing some operating margin due to supply chain shocks will likely also affect its competitors. Hence, I am assured that Murata Manufacturing is likely the most investment-worthy of the big parts-manufacturers in Japan.

2. Opportunities and Risks

In the fiscal year of 2023 of Murata, ending March 31, 2023, the company forecasts an increase in sales and a decrease in profit. The assumed exchange rate is 120 yen to the dollar, and the exchange rate sensitivity is 11 billion yen per yen for U.S. dollars, net sales of 11 billion yen/year, and operating income of 6 billion yen/year.

Opportunities

As the rate now is 147 yen to the dollar, we’ll likely see much higher increase in both profits and costs. However, as has large manufacturing capacity in Japan, the rapid yen depreciation will likely have a positive short-term effects on its profits.

Long-term, an expansion of markets for telecommunications, automobiles, IoT products, etc. are a given. That Murata is able to uphold a profit margin higher than its peers shows that its products are hardly replacable and likely not at risk of disruption.

Murata is also investing rapidly in increasing its product lineup and improving productivity and combatting an aging workforce through smart-factory initiatives. Recently, the company has increased production capacity through M&A initiatives, mainly ETA Wireless. With Murata’s large cash reserves in a market where liquidity is drying up, I believe this is a great strategy for further growth.

Risks

As the latest financial report from Murata has shown, there are major business risks short-term. The largest risk is the deterioration of market conditions due to global economic stagnation and geopolitical risks. On top of that, with Murata’s high profit margins, there is always a risk of intensification of competition in the most profitable segments.

Also, one of Murata’s largest client’s, Apple, is shifting to focus on a more software based strategy and already decreasing its proudction of smartphones and PCs. This will hurt Murata’s bottom line both short-term and long-term, but the company will likely find other clients to make up for it.

Lastly, both Murata’s biggest outside market and production center, China, is seeing a deterioration of market conditions due to worsening economic and political conditions. Murata is well-equipped for this as the company is increasing production outside of China, especially in Japan, but it is a tough shift that will cause damages to its bottom line.

3. Financial soundness

Next, let's look at the financial situation. This is the situation as of the end of June 2022:

Total assets: ¥2,850.2 billion

Total liabilities: ¥522.7 billion

Total net assets: ¥2,327.5 billion

Equity ratio: 81.7%

Interest-bearing debt: ¥111 billion

Interest-bearing debt ratio: 4.8%

Current ratio: 489%

Cash and deposits: ¥348.9 billion

The financial situation is very good. The equity ratio, interest-bearing debt ratio, and current ratio all indicate a well-funded business, and any bankruptcy risk is low, even if interest rates go up substantially.

However, as Murata is in a very cash intensive industry, these numbers could quickly shift as interest rates goes up.

4. Stock-price

The stock price as of October 4, 2022 is 6,790 yen.

In the 6-month chart, it is gradually declining. In addition to concerns about an economic slowdown, Apple's plan to increase iPhone production was recently postponed, so the company, which is an affiliated company, also fell sharply.

However, in the 10-year chart, we can see that the stock has had a remarkable journey. This is a reflection on its outperformance to its peers when it comes to consistently growing both earnings and profit margins. Hence, when the economy stabilize again, we’ll likely see a continuing journey upwards.

Indicators

Market capitalization: ¥4,692.2 billion

Price/Earnings ratio (estimate): 13.65x

Price/Book ratio: 1.89x

With a market capitalization of ¥4,692.2 billion yen, Murata is definitely a large cap company is the same size as Japanese giants like JT (Japan Tobacco) and Canon.

From a P/E ratio perspective, the stock is slightly overvalued, especially considering the P/E is measured for the company’s record year of FY22.

From a P/B perspective, the stock also looks slightly overvalued. However, this is likely due to Murata valuing their intangible assets relatively modestly.

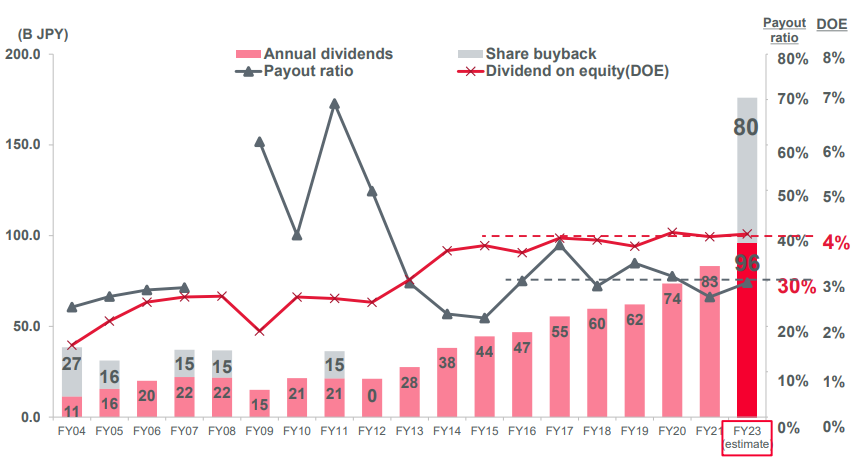

5. Dividends & Share-buybacks

Dividends have increased every fiscal year since 2017. With a dividend payout ratio of around 30% and a dividend yield of 2.12%, Murata gives out good dividend for a company still in its growth phase, while

Murata’s leadership has also included a large share buyback program from April 22, 2022. This program will buy up to 2.5% of all outstanding stocks which will likely have a positive push up on the stock. However, the does not seem to stop the drop in share-price as it has fallen more than 25% YTD.

The company does project higher dividend and share-buybacks in the future, but as profits look to decrease this year, this might be a bit too optimistic to hope for.

6. Conclusion

Judging Murata Manufacturing Co., Ltd. comprehensively, I think that it is an excellent company ready to take on the increasing manufacturing demand from Japan. Long-term, the future prospects, profitability, and financial situation are all good. It is a company that you want to consider purchasing at a low price in the long run.

However, in the short-run, the company does suffer from the same supply-chain shortages, increasing electricity prices and slump in demand as the rest of the industry. With a P/E of over 13 on the previous year’s record earnings, I still think the stock has some room to fall before it’s worth buying.

Therefore, this stock is definitely on my buying radar, but I’d wait until it falls a bit more before picking it up.