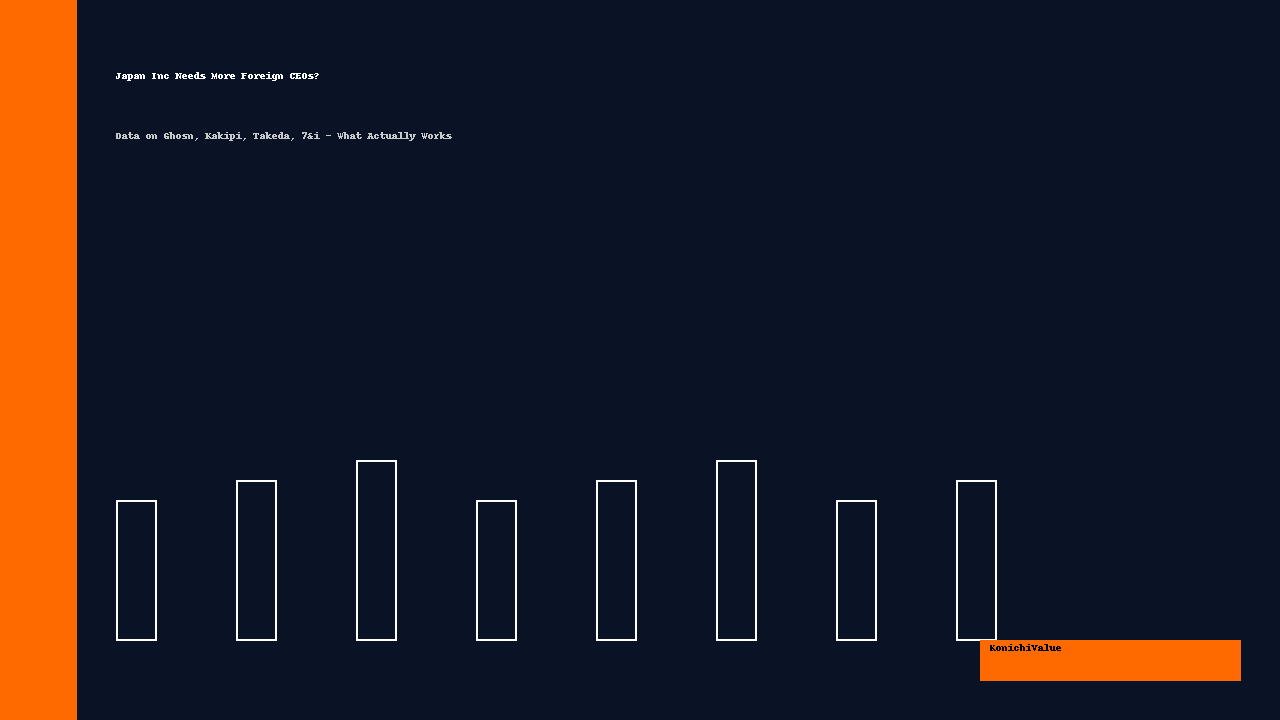

I’ve long argued that Japan’s corporate problem isn’t a lack of talent; it’s a lack of outside air.

When boards finally crack a window and hire a foreign chief, headlines swing between “savior” and “scandal.” So: are foreign leaders good for Japan Inc, or just good copy? Let’s look at results: