How Inflation is Wiping Out Japan's National Debt

Is the Japanese government paying off their debt at the cost of their population?

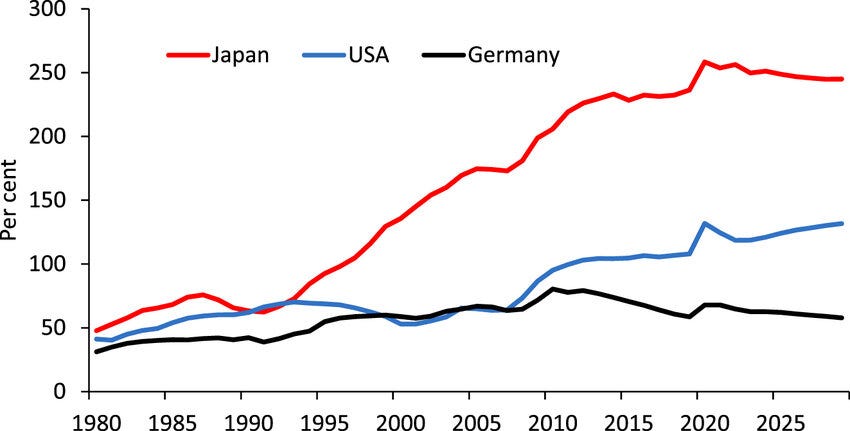

Japan is the undisputed heavyweight champion of national debt.

The numbers are so large they almost lose their meaning. We are looking at a nominal gross domestic product of roughly 665 trillion yen as of 2025, stacked against a gross government debt of 1,342 trillion yen. Depending on the metric, the government debt-to-GDP ratio sits between 230% and a …