Disclaimer: The information in this stock-analysis represents my opinions and should not be construed as personalized or individualized investment advice, and are subject to change.

I've been on a mission to find some hidden gems in the stock market, and guess what? After digging deep into the Tokyo Stock Exchange and screening for the most undervalued stocks, I kept stumbling upon one name: Fujikura Ltd. (TYO 5803). This Japanese conglomerate has been around since 1885 and has its fingers in a bunch of different sectors worldwide. But for some reason, it's still flying under the radar for a lot of investors.

I understand your skepticism: there must be a catch. Indeed, Fujikura faces geopolitical risks, such as operations in volatile regions like Ukraine. Additionally, its diversified portfolio presents a double-edged sword. While it provides a hedge against downturns in individual sectors, it also complicates matters for investors attempting to comprehend the company's potential and synergies between its various businesses.

However, Fujikura is steadfast in its commitment to innovation, aggressively expanding its optical wiring solutions division. They are even at the forefront of pioneering photonics-electronics convergence technology known as "IOWN." If one can see beyond the inherent complexities and potential hazards, there lies an undervalued stock with immense potential—boasting an astonishingly low P/E ratio of 4.2.

In the subsequent text, we will delve deeper into Fujikura's realm, examining its core business segments and groundbreaking products. We will investigate the challenges and risks that may be suppressing the stock's value while unveiling the concealed opportunities that make it so enticing for discerning investors. Join us as we embark on an insightful journey to uncover the remarkable potential of Fujikura Ltd.

Overview of Company

Fujikura Ltd. (TYO 5803) is a diversified Japanese conglomerate with a rich history dating back to its founding in 1885. The company operates in various sectors, including energy, telecommunications, electronics, automotive, and real estate, both in Japan and internationally. Fujikura is relatively known in Japan for its innovative and high-quality products and services.

Fujikura's core strength lies in its four main business segments: Power & Telecommunication Systems, Electronics Business, Automotive Products Business, and Real Estate Business. The company manufactures and supplies a wide range of products, such as twisted pair cables, coaxial cables, eco cables, conductors, OHTL and power cables, optical fibers/fiber cables, splicers and others, optical components, MDC/MMC solutions, specialty fibers, optical applied products, and fiber lasers.

While Fujikura's products and services are highly regarded, the stock may be overlooked by some investors due to its exposure to multiple industries and businesses in countries like Ukraine, which face geopolitical risks and uncertainties. The current political and economic environment in Ukraine, for instance, may hamper investors' expectations and lead them to undervalue Fujikura's growth potential.

Moreover, Fujikura's diversified portfolio of businesses and industries can be both a blessing and a curse. On one hand, the company's broad range of products and services provides a strong foundation and hedges against downturns in individual sectors. On the other hand, this diversification might make it challenging for investors to fully grasp the company's potential and synergies between its various businesses. As a result, the stock could be flying under the radar, presenting a hidden opportunity for those willing to delve deeper into Fujikura's operations.

Despite these challenges, Fujikura's commitment to innovation and expanding its optical wiring solutions business, as well as its involvement in developing groundbreaking photonics-electronics convergence technology "IOWN," positions the company for future growth. Investors who can look past the complexities of Fujikura's diverse businesses and the potential risks associated with its operations in countries like Ukraine may discover a significantly undervalued stock with immense potential.

Table of Contents

KonichiValue Score

Profitability

Opportunities & Risks

Financial Soundness

Dividend

Stock-price

Conclusion

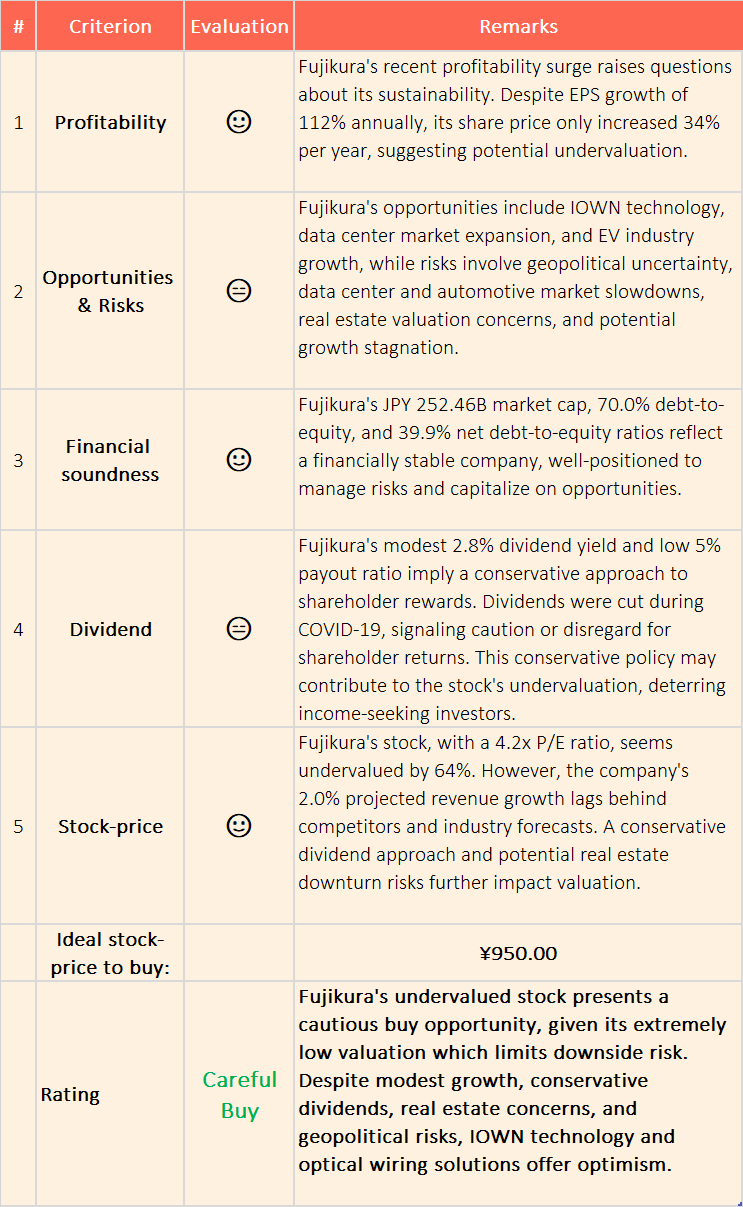

0. KonichiValue Score

1. Profitability

Fujikura's profitability has seen a remarkable turnaround in recent years. The third quarter of 2023 witnessed a surge in revenues, exceeding analysts' expectations by 3.8%. However, the earnings per share (EPS) trailed behind, missing estimates by 38%. The company's net income and profit margin experienced significant growth, with the latter rising from 5.4% in 3Q 2022 to 6.9% in 3Q 2023.

Over the last three years, Fujikura's EPS has skyrocketed by an astounding 112% annually. Yet, its share price has only increased by 34% per year, indicating a potential undervaluation of the stock. A review of Fujikura's historical financial performance sheds light on the company's growth trajectory and profitability over the past five years:

Sales decreased from JPY 7,400 billion in FY2017 to JPY 6,437 billion in FY2020, but rebounded to JPY 6,703 billion in FY2020.

Operating profit declined from JPY 343 billion in FY2017 to JPY 244 billion in FY2020, before surging to JPY 383 billion in FY2020.

Net income experienced high volatility, ranging from JPY 183 billion in FY2017 to a negative JPY 385 billion in FY2019, before recovering to a positive JPY 391 billion in FY2020.

The question is if this profit growth is sustainable in the long run?

2. Opportunities & Risks

Fujikura's future is laden with opportunities and challenges. In order to provide a comprehensive analysis, let's delve deeper into the key factors driving the company's growth and potential risks:

Opportunities:

Photonics-Electronics Convergence Technology "IOWN": Fujikura's involvement in the groundbreaking "IOWN" project, led by Nippon Telegraph and Telephone Corporation (NTT), positions the company at the forefront of next-generation communication technology. NTT has committed to investing JPY 500 billion ($4.4 billion) over the next five years to develop IOWN. By focusing on strengthening its optical wiring solutions business and developing new markets and customers globally, Fujikura can capitalize on the growing demand for advanced communication infrastructure.

Data Center Market Expansion: Despite the recent economic slowdown in the data center market, the long-term outlook remains positive. The global data center market is projected to grow at a CAGR of 6.1% from 2021 to 2028, reaching $267.3 billion by 2028. As the world continues to generate, store, and process vast amounts of data, the need for efficient data centers will only increase. Fujikura's expertise in optical fiber technology and solutions enables the company to capture a significant share of this growing market.

Electric Vehicle (EV) and Automotive Industry Growth: Fujikura's automotive components, wires, and wire harnesses position the company to benefit from the continued growth of the EV market and the broader automotive industry's ongoing recovery. The global EV market is expected to grow at a CAGR of 29.7% from 2021 to 2028, reaching $2.49 trillion by 2028. By focusing on innovation and developing products tailored for the evolving needs of automakers, Fujikura can establish itself as a key supplier in this high-growth sector.

Positive outlook from leadership: “By segment, the Fujikura leadership expect record high sales, operating income, and ordinary income for FY2023. Even though losses in the automotive business sector will increase, they believe the electronics business sector will recover it.

Risks:

Geopolitical Risks and Economic Uncertainty: Fujikura's operations in countries like Ukraine expose the company to potential geopolitical risks and economic uncertainties. In 2021, Fujikura reported approximately JPY 17 billion ($150 million) in sales from its Ukrainian operations. The current political and economic climate in these regions can hamper investors' expectations and lead to undervaluation of the company's growth potential. Moreover, any escalation in geopolitical tensions may adversely impact Fujikura's operations, profitability, and reputation.

Slowdown in the Data Center Market: The recent economic slowdown in the data center market poses a significant risk to Fujikura's growth prospects. With increased competition and potential saturation in some regions, the company may struggle to achieve its growth targets in this crucial sector. For instance, the data center market in North America experienced a slowdown in 2021 due to oversupply and high levels of speculative development. Moreover, any disruptions in the global supply chain, such as soaring transportation costs or component shortages, could further exacerbate the slowdown.

Slowdown in the Automotive market: The Fujikura leadership has announced that the global automotive market will see a slowdown and this sector might not recover for years, which will be a heavy burden on the company’s third largest segment.

Lower valuations in real-estate: Fujikura's real estate segment represents a considerable portion of its diversified portfolio. The company owns and manages various properties, including commercial and residential buildings. However, this segment may not have a clear synergy with Fujikura's other business areas, such as optical wiring solutions, electronics, and telecommunications. The lack of synergy could lead to management inefficiencies and suboptimal allocation of resources. This segment will likely see a serious correction in the coming quarters. There is a high risk that the company will lose a lot of its asset valuation if real-estate does not recover in the coming quarters.

Stagnation in Growth: Fujikura's diversified portfolio of businesses and industries, while providing a strong foundation, could also contribute to stagnation in growth over the next few years. The complexity of managing multiple businesses and the need to invest in various sectors may dilute the company's focus and resources, limiting its ability to capitalize on high-growth opportunities. As a result, Fujikura may face difficulties in achieving the ambitious revenue growth forecast of 2.0% p.a. on average during the next three years.

3. Financial Soundness

Fujikura's market capitalization of JPY 252.46 billion and a debt-to-equity ratio of 70.0% signify a financially sound company with a stable footing in the industry. The net debt-to-equity ratio of 39.9% is considered satisfactory, further bolstering Fujikura's financial standing. These strong financials provide a solid foundation for the company to navigate the potential risks and seize upcoming opportunities.

4. Dividend

Fujikura's current dividend yield stands at a modest 2.8%, with a surprisingly low payout ratio of just 5%. The company's dividend history demonstrates a conservative approach to rewarding shareholders, with dividends per share increasing from JPY 0 in FY2020 to JPY 10 in FY2020. However, during the Covid-19 pandemic, the company slashed its dividend, indicating a cautious stance or even a lack of concern for shareholder returns during challenging times. This conservative dividend policy might be one of the factors contributing to the stock's undervaluation.

On the positive side, the low payout ratio suggests that Fujikura has enormous capacity for dividend increases in the future. As the company continues to grow and strengthen its financial position, it could potentially increase its dividends, thereby improving shareholder returns and making the stock more attractive to income-seeking investors.

5. Stock Price: Cheap or Expensive?

Fujikura's stock is notably cheap with a P/E ratio of 4.2x, compared to its estimated fair value of 12.1x, as calculated by the 2-stage DCF model. This implies a 64% undervaluation, suggesting the market may not be accounting for the company's full potential.

However, reasons for this undervaluation exist. Analyst forecasts predict a meager 2.0% p.a. average revenue growth for Fujikura over the next three years, contrasting with the 5.2% growth forecast for Japan's Electrical industry. Competitors like Mabuchi Motor (TYO: 6592), GS Yuasa (TYO: 6674), and Ushio (TYO: 6925) are experiencing faster growth and innovation.

These competitors outpace Fujikura by targeting high-growth market segments and investing in R&D to stay ahead. Fujikura's internal forecasts and market conditions suggest the company is struggling to capitalize on high-growth opportunities. A low dividend yield of 2.8% and a 5% payout ratio indicate a conservative approach or disinterest in rewarding shareholders, further affecting the stock's valuation.

On top of that, the company has a big bet on real-estate which is. In the likely event of a downturn, the real estate segment might experience reduced rental income, increased vacancies, and a decline in property values. Consequently, Fujikura's overall asset valuation could be negatively impacted, potentially leading to a decline in its stock price. Moreover, real estate investments require significant capital, and divesting from such properties can be a slow and complex process, further exacerbating the risks associated with this segment. It is essential for investors to consider these factors when evaluating Fujikura's potential as an investment.

In conclusion, Fujikura's stock appears cheap, but its undervaluation has valid reasons. Investors should carefully consider the company's growth potential against industry peers and market dynamics before taking a position in this seemingly attractive investment.

Ideal Stock-Price to Buy: ¥950

6. Conclusion

Fujikura (TYO 5803) presents a unique investment opportunity for those willing to tread carefully. The company's stock appears significantly undervalued, which might be alluring to value-oriented investors. However, several factors contribute to its cheap valuation and may continue to suppress its price:

First, Fujikura's growth prospects are relatively modest compared to its competitors, such as Mabuchi Motor, GS Yuasa, and Ushio. These companies have successfully leveraged high-growth market segments and invested in R&D to drive innovation, outpacing Fujikura in the process. Analyst forecasts predict a mere 2.0% p.a. average revenue growth for Fujikura over the next three years, compared to the 5.2% growth forecast for the overall Japanese Electrical industry.

Second, Fujikura's conservative dividend policies and low payout ratio of just 5% suggest that the company either lacks interest in rewarding shareholders or is overly cautious. This factor may deter income-seeking investors and contribute to the stock's low valuation.

Third, Fujikura’s real-estate bets do not seem to provide any synergies to the rest of its segments and with increasing interest rates and the coming downturn in the market, it might be a burden that puts pressure on the company's overall valuation.

Last, geopolitical risks, such as the company's business in Ukraine, may hamper investor expectations and further depress the stock price.

Despite these challenges, Fujikura's strategic focus on strengthening its optical wiring solutions business, expanding globally, and potentially contributing to the development of photonics-electronics convergence technology "IOWN" offers some optimism for future growth.

In light of these factors, Fujikura's stock can be considered a careful buy, but because of its big real-estate investment, disregard for shareholders and low growth prospects, I would be very careful to bet big. However, with the incredibly low P/E of 4.2 for a highly profitable company, I’d still argue that the downside is incredibly low.

As with any investment, thorough research and due diligence are essential in determining whether Fujikura's undervalued stock is a hidden gem or a value trap.